What is E-Invoicing: Complete Guide to GST E-Invoice System, Meaning, Rules, Benefits & Applicability

Summary

E-invoicing under GST is a mandatory system where B2B invoices are electronically validated through the Invoice Registration Portal (IRP) to generate a unique IRN, making them legally valid. It applies to businesses with turnover above ₹5 crore and ensures real-time tax compliance, auto-reporting in GST returns, and improved transparency. The system reduces errors, prevents tax evasion, and streamlines operations, but requires timely reporting (within 30 days) to avoid penalties and loss of ITC eligibility.

Table of Content

- Introduction to E-Invoicing Under GST

- Understanding E-Invoicing Fundamentals

- Invoice Registration Portal (IRP): Role and Workflow

- E-Invoicing Applicability and Requirements

- Mandatory Data Fields and Components of E-Invoice

- Step-by-Step E-Invoice Generation Process

- E-Invoice vs Traditional Invoice: Key Differences

- Compliance Deadlines and Reporting Timelines

- Common Challenges and Solutions in E-Invoicing

- Benefits and Impact of E-Invoicing for Businesses

- Penalties for Non-Compliance with E-Invoice Rules

- Conclusion and Next Steps for GST E-Invoicing

- Additional Resources and LOGIC ERP Integration Options

Introduction

E-invoicing under GST is the mandatory electronic reporting of business to business invoices to the Invoice Registration Portal (IRP), where each invoice receives government authentication before becoming a valid tax document. This e invoice system transforms how registered persons handle B2B transactions by requiring real-time verification through the central tax network. Governments are increasingly mandating e-invoicing for B2B transactions to improve tax reporting and compliance.

This guide covers GST e-invoice rules, applicability criteria based on aggregate turnover, mandatory data fields in the prescribed schema, the step-by-step process to prepare e invoice documents, and penalties for non-compliance. The content addresses GST-registered businesses, tax professionals, and enterprises with annual turnover above Rs. 5 crore who need clarity on e invoicing rule requirements. Understanding these requirements matters because invoices without valid IRN cannot be used for input tax credit claims, and non-compliance triggers significant financial penalties under GST law.

Direct answer: E-invoicing is the mandatory electronic authentication of business invoices through the Invoice Registration Portal IRP, which validates invoice data, assigns a unique invoice reference number (IRN), and returns a digitally signed JSON format response with a QR code making the document legally valid under the GST system. This is commonly referred to as an e-invoice in industry discussions and GST regulations. E-invoicing is the process of reporting B2B invoices to the IRP to obtain a unique IRN, which is necessary for issuing valid invoices to customers.

Key outcomes from this guide:

- Understanding e invoice meaning and its distinction from regular digital invoicing

- Knowing exact turnover threshold and applicability criteria for notified taxpayers

- Mastering mandatory field requirements and e invoice schema specifications

- Implementing the complete process to generate IRN through billing software integration

- Avoiding penalties and protecting ITC eligibility through proper compliance

Historical Background and Evolution of E-Invoicing

The journey of e-invoicing, or electronic invoicing, in India is closely tied to the country’s broader push for digital transformation and tax compliance. While digital invoicing solutions began gaining traction globally in the early 2000s, it was the introduction of the Goods and Services Tax (GST) regime that set the stage for a standardized e invoice system in India.

Recognizing the challenges of manual errors, tax evasion, and inconsistent invoice formats, the GST Council initiated the e-invoicing rule as a cornerstone of its compliance strategy. The goal was to create a unified process where every GST invoice issued by notified taxpayers would be authenticated in real time, ensuring transparency and traceability across the entire supply chain.

A pivotal milestone in this evolution was the launch of the Invoice Registration Portal (IRP), commonly referred to as the e invoice portal. This centralized platform enables businesses to upload invoice details in a prescribed schema, receive a unique invoice reference number (IRN), and obtain a digitally signed response complete with a QR code. The IRP’s integration with the GST portal and e way bill portal further streamlined compliance, allowing for seamless auto generation of e way bills and auto population of GST returns.

Over time, the government has refined the e-invoicing framework to balance robust compliance with ease of use. The e invoicing rule initially applied to large enterprises but has gradually expanded to cover businesses with an aggregate turnover above Rs. 5 crore. This phased approach ensures that both large corporations and small businesses can adapt to the system without undue burden. Notified taxpayers are now required to prepare e invoices in a standardized format, capturing essential invoice details such as invoice number, date, supplier GSTIN, line items, and invoice value.

Technological advancements have played a crucial role in this evolution. The adoption of the JSON format for e invoice schema has made it easier for billing software to generate and validate invoices, reducing manual intervention and the risk of errors. The use of digital signatures and QR codes embedded in each invoice allows tax authorities to instantly verify authenticity, further minimizing opportunities for tax evasion.

The system’s flexibility is evident in its ability to accommodate a wide range of business scenarios. Whether dealing with bonded warehouse sales, high sea sales, warehousing zones, or partial cancellation of invoices, the e invoice system is designed to handle diverse document types including debit notes and credit notes while maintaining compliance with GST law. The auto population of invoice data into GST returns and the auto generation of IRN details have significantly reduced the compliance workload for businesses.

Throughout this evolution, the GST Council has remained proactive, regularly updating the prescribed schema and compliance thresholds to reflect changing business needs and technological capabilities. The result is a robust, scalable e-invoicing ecosystem that not only curbs tax evasion but also enhances operational efficiency for businesses of all sizes.

As India’s economy continues to digitize, the e-invoicing system is expected to become even more integral to business operations. Its standardized approach, real-time validation, and seamless integration with the GST system position it as a key driver of transparency, compliance, and growth in the digital era.

Understanding E-Invoicing Fundamentals

E-invoicing under GST is a government authentication system where registered persons must upload invoice details to an authorized e invoice portal before an invoice becomes valid for tax purposes. Unlike simply creating electronic documents, this system requires real-time validation through the services tax network infrastructure.

The core purpose extends beyond documentation e-invoicing prevents tax evasion by ensuring every B2B invoice issued enters the government database immediately, enabling tax authorities to verify transactions and identify fraudulent ITC claims before they impact revenue collection.

Core Components of E-Invoice System

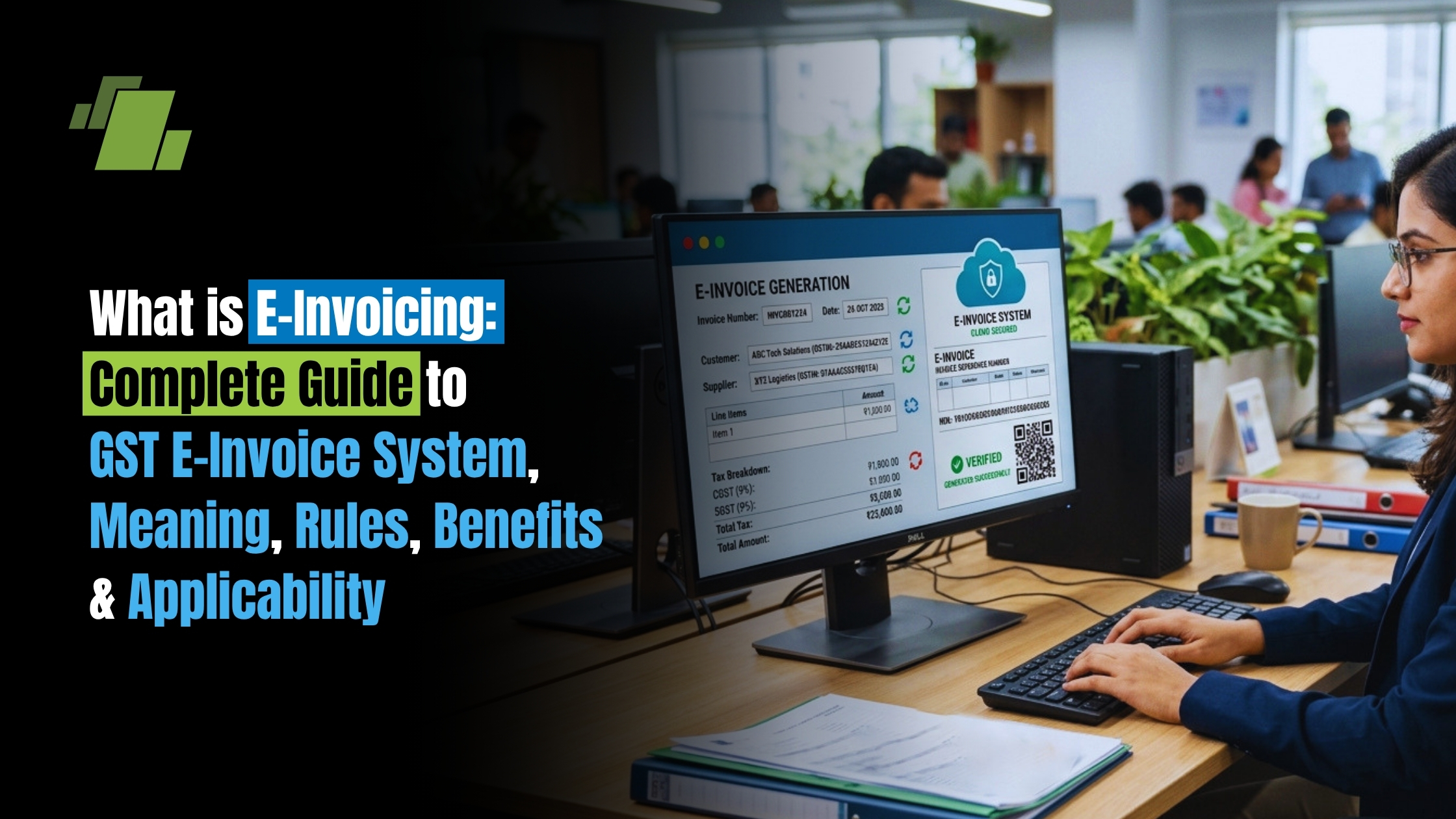

The Invoice Registration Portal IRP serves as the central authentication hub where all e invoice data flows. When a registered person uploads invoice details in the prescribed schema, the IRP validates approximately 132 data fields, checks for duplicates against existing records, and verifies master data accuracy including supplier GSTIN, recipient information, and HSN codes.

Upon successful validation, the portal generates a unique invoice reference number IRN a 64-character alphanumeric identifier that makes each document uniquely traceable within the GST system. This invoice reference number IRN gets embedded into the returned JSON format response along with a QR code containing the digital signature of the IRP.

The connection between these components creates an unbroken chain: without IRP validation generating a valid IRN, the document lacks legal standing as a GST invoice, and recipients cannot claim input tax credit regardless of whether payment occurred.

E-Invoicing Under GST Framework

The e invoice system integrates directly with GST return filing through auto population features. When invoice data receives authentication, it automatically feeds into GSTR-1 sales returns, eliminating manual errors in reporting and ensuring consistency between invoices and declared supplies. All invoice and supply details must be accurately captured and reported within each designated tax period for compliance and proper filing.

This real-time authentication means the GST portal receives invoice information at the moment of generation not weeks later during return filing. Tax authorities gain immediate visibility into transaction patterns, taxable value declarations, and supply chains across registered persons.

Understanding these fundamentals establishes why specific applicability rules matter the government targets transactions where authentication provides maximum compliance benefit.

GST System and E-Invoicing: Integration and Interactions

The integration of the GST system with e-invoicing has revolutionized how businesses manage and report their invoice data, ensuring seamless compliance and transparency across the entire tax ecosystem. At the heart of this integration is the Invoice Registration Portal (IRP), which acts as the official gateway for authenticating every e invoice issued by notified taxpayers.

When a business prepares an e-invoice, the invoice details including invoice value, taxable value, and all required line items are structured according to the standardized e invoice schema. This schema, mandated by the GST council, ensures that every invoice follows a uniform format, minimizing manual errors and making it easier for both businesses and tax authorities to process and verify invoice data.

Once the invoice is ready, it is uploaded to the IRP, where it undergoes real-time validation. The IRP checks the invoice against GST system master data and, upon successful verification, generates a unique invoice reference number (IRN). This IRN is essential for GST compliance, as it authenticates the invoice and prevents the creation of duplicate or fraudulent invoices. The IRP also embeds a QR code into the e-invoice, which can be scanned to instantly verify the authenticity of the invoice an important safeguard against tax evasion.

The GST portal is closely linked with the e-invoice system, enabling auto-reporting of invoice data directly to the tax authorities. This integration means that once an invoice is validated and assigned an IRN by the IRP, the invoice details are automatically populated into the relevant GST returns, such as GSTR-1. This auto population feature not only streamlines compliance but also significantly reduces the risk of manual errors that can occur during data entry.

Additionally, the e-way bill portal is integrated with the e-invoice system, allowing businesses to generate e-way bills and e-invoices in a single workflow. This is particularly beneficial for businesses involved in goods transport, as it ensures that all necessary documentation is in place for the movement of goods, further supporting GST compliance.

The e-invoicing rule applies to notified taxpayers whose aggregate turnover exceeds the prescribed threshold set by the GST council. These businesses are required to prepare e-invoices in the standardized format and obtain a valid IRN from the IRP before issuing the invoice to their customers. This rule is designed to bring greater transparency to business transactions and to curb practices such as high sea sales and bonded warehouse sales that have historically been used for tax evasion.

The GST law also provides for partial cancellation of invoices through the IRP, allowing businesses to correct errors without issuing entirely new documents. This flexibility, combined with the robust integration between the GST system, IRP, and e-way bill portal, ensures that businesses can maintain accurate and compliant invoice records throughout each tax period.

In summary, the close integration between the GST system and the e-invoice system anchored by the invoice registration portal IRP creates a streamlined, transparent, and secure environment for managing business invoices. By leveraging standardized formats, unique invoice reference numbers, QR codes, and auto-reporting features, the GST ecosystem not only reduces manual errors but also strengthens compliance and significantly curbs tax evasion. For notified taxpayers, adhering to these integrated processes is essential for maintaining GST compliance and supporting the broader goals of the GST regime.

E-invoicing Process

E-invoicing provides better data management, enabling instant access to financial data for cash flow forecasting. Automated workflows in e-invoicing speed up approval times and payments. Digital invoices are typically encrypted and authenticated with digital signatures, enhancing security. The process of e-invoicing includes generation, validation, authentication, transmission, and final delivery.

E-invoicing Applicability

E-invoicing does not apply to certain entities such as insurers, banking companies, financial institutions, and government departments, among others.

Invoice Registration Portal (IRP): Role and Workflow

The Invoice Registration Portal (IRP) is the backbone of the GST e-invoice system, serving as the official gateway for authenticating and registering every GST invoice issued by notified taxpayers. Its primary function is to validate invoice details, assign a unique invoice reference number (IRN), and ensure that each e invoice is both authentic and compliant with GST law before it enters the GST system.

When a business prepares an e invoice using its billing software, the invoice data including the invoice number, invoice value, taxable value, and all required line items must be uploaded to the IRP in the standard format prescribed by the GST Council. This process is crucial for businesses dealing with high transaction volumes, such as goods transport agencies, financial institutions, and companies operating in warehousing zones, as it ensures every invoice is reported accurately and efficiently.

How the Invoice Registration Portal IRP Works:

- Invoice Generation: The supplier creates the GST invoice in their billing software, ensuring all invoice details are complete and formatted according to the prescribed e invoice schema.

- Invoice Upload: The invoice data is transmitted to the IRP, typically in JSON format, including the unique invoice number, date, supplier and recipient GSTINs, invoice value, and taxable value.

- Verification: The IRP cross-checks the invoice details against the GST system’s master data, validating GSTINs, document numbers, and other critical fields to prevent manual errors and tax evasion.

- IRN Generation: Upon successful verification, the IRP generates a unique invoice reference number IRN a 64-character alphanumeric code that makes the invoice uniquely traceable.

- QR Code Generation: The IRP also creates a QR code containing the IRN, invoice value, taxable value, and other essential invoice data, digitally signed for authenticity.

- Auto-Reporting to GST Portal: The authenticated invoice, along with its IRN and QR code, is automatically reported to the GST portal, enabling seamless auto population of GST returns and reducing manual intervention.

The IRP also supports partial cancellation of invoices, allowing businesses to correct errors without generating entirely new documents an essential feature for minimizing discrepancies and maintaining accurate records.

E-Invoicing Applicability and Requirements

Building on the authentication framework, specific rules determine which businesses must comply with e invoicing requirements and which transactions fall within mandatory coverage.

Turnover Threshold and Eligibility

The current prescribed threshold requires e-invoicing for any registered person whose aggregate turnover exceeded Rs. 5 crore in any financial year since FY 2017-18. This turnover calculation considers all GSTINs under the same PAN, including exempt supplies and export transactions not just taxable supplies.

Critically, the “once above, always above” principle applies: if a business crossed the turnover threshold in any previous year, e invoicing rule applies permanently regardless of current revenue levels. A company with Rs. 8 crore turnover in FY 2022-23 but only Rs. 3 crore in the current year must still comply.

The rule applies specifically to:

- Business to business supplies (invoices to GST-registered recipients)

- Export invoices and deemed exports

- Supplies to government departments and entities (B2G)

- Supplies to SEZ developers (not SEZ units themselves)

Excluded Entities and Transactions

Certain notified class categories remain exempt from e-invoicing regardless of their aggregate turnover:

Exempt business categories:

- Banks and financial institutions

- Insurance companies

- Non-banking financial companies (NBFCs)

- Goods transport agency operators

- Passenger transport service providers

- Government departments and local authorities

- SEZ units (developers remain covered)

- Multiplex cinema admission service providers

Excluded transaction types:

- B2C sales to unregistered consumers

- High sea sales and bonded warehouse sales

- Free trade warehousing zones transactions

- Reverse charge supplies (where recipient pays tax)

- Import transactions

Excluded document type categories:

- Delivery challans

- Bills of supply for exempt goods

- Bill of entry documents

- Input Service Distributor (ISD) invoices

- Job work challans

Mandatory Data Fields and Components

The e invoice schema contains approximately 132 total fields, with around 28 absolutely mandatory and 18 conditionally mandatory based on transaction nature. Missing or incorrect mandatory fields cause immediate rejection by the IRP.

Essential information categories include:

Supplier details: Legal name, complete address, supplier GSTIN, state code, PIN code, and registration status.

Recipient data: Recipient GSTIN (mandatory for B2B), legal name, shipping address, destination state, and PIN code mapping.

Invoice specifics: Unique document number (cannot repeat within the financial year for that supplier), invoice date in correct format, document type code (INV for invoice, CRN for credit note, DBN for debit note), and supply type classification.

Line items information: HSN or SAC code for each item, description, quantity with unit quantity code, unit rate, and item-level taxable value.

Tax calculations: Tax rates, CGST/SGST/IGST amounts, cess if applicable, total invoice value, and applicable discounts.

Payment information: Mode of payment, bank account details when relevant, and credit period if extended.

The IRP validates these fields against master data incorrect state-PIN mapping, invalid HSN codes, or mismatched GSTIN formats trigger rejection before IRN generation.

E-Invoicing Process and Implementation

With applicability criteria and field requirements established, the actual process to prepare e invoice documents follows a structured flow from creation through authentication.

Step-by-Step E-Invoice Generation Process

This process applies whenever a presently covered business creates any B2B invoice, debit note, or credit note for a registered recipient.

- Generate invoice in billing software: Create the invoice with all mandatory fields populated, ensuring document number uniqueness within the financial year, correct HSN codes, and accurate recipient GSTIN.

- Upload to IRP via Form GST INV 01: Transmit the invoice data in standardised format through API connectivity, GSP/ASP integration, or the offline tool the JSON format must match the prescribed schema exactly.

- Receive IRN and QR code: Upon validation, the IRP returns a digitally signed response containing the unique invoice reference number and QR code embedded with core transaction data and the portal’s digital signature.

- Print and issue with authentication details: The final invoice issued to the recipient must display the IRN details and QR code this authenticated version becomes the legally valid document for GST purposes.

Important timing requirement: From April 1, 2025, businesses with annual turnover of Rs. 10 crore or above must upload invoices to the IRP within 30 days of the invoice date. Documents beyond this time limit face automatic rejection, making the invoice invalid for ITC claims.

E-Invoice vs Traditional Invoice Comparison

| Criterion | Traditional Invoice | E-Invoice |

|---|---|---|

| Authentication method | Self-generated by supplier | Government-validated through IRP |

| Government verification | None at creation | Real-time validation with IRN |

| Unique identifier | Invoice number only | Invoice number + unique invoice reference number |

| GST compliance validity | Based on format compliance | Based on IRP authentication |

| ITC eligibility for buyer | Subject to recipient verification | Automatic through GST portal integration |

| GST return population | Manual entry required | Auto reporting to GSTR-1 |

| Legal standing under GST law | Depends on format compliance | Confirmed through valid IRN |

This comparison clarifies why businesses dealing with eligible transactions cannot treat e-invoicing as optional traditional invoices lacking valid IRN fail GST compliance requirements entirely for covered transactions.

Timeline and Compliance Deadlines

The 30-day reporting requirement effective April 1, 2025 applies to notified taxpayers with Rs. 10 crore or above annual turnover. This time limit creates operational urgency invoices must reach the IRP within the window or become permanently rejected.

Consequences of delayed reporting include:

- IRP rejection with no option to obtain IRN for that document

- Invoice treated as invalid under CGST rules

- Recipient unable to claim input tax credit

- Potential penalty exposure under Section 122

For credit note and debit note documents, the same 30-day rule applies late reporting invalidates the adjustment regardless of commercial legitimacy.

Common Challenges and Solutions

Businesses transitioning to e-invoicing encounter predictable obstacles that proper preparation can address.

Technical Integration Issues

Solution: Establish IRP connectivity through ERP or billing software API integration before compliance deadlines. Most modern accounting systems offer built-in e invoice portal connections or third-party middleware options. Test connectivity with sample transactions, verify JSON format output matches the prescribed schema, and establish fallback procedures for e way bill portal integration when goods transport requires coordinated documentation.

Data Accuracy and Field Validation

Solution: Implement pre-submission validation checks against known rejection triggers. Common errors include state-PIN code mismatches, invalid HSN codes from outdated master lists, incorrect recipient GSTIN formats, and document number duplication across financial year boundaries. Build data hygiene processes that verify supplier GSTIN accuracy, validate address components against government master data, and flag incomplete line items before IRP upload attempts.

Staff Training and Change Management

Solution: Document the complete process from invoice creation through IRN receipt, identifying decision points and error recovery procedures. Train relevant staff on mandatory field requirements, explain why partial cancellation or amendment rules differ from traditional invoicing, and establish escalation paths for rejection handling. Regular refresher sessions address schema updates and validation rule changes that GSTN implements periodically.

Benefits and Impact of E-Invoicing

Beyond compliance necessity, the e invoice system delivers measurable improvements for tax administration and business operations. E-invoicing can lead to up to 90% cost savings compared to paper invoices. Switching to e-invoicing can cut paper usage by up to 90%, contributing to sustainability goals.

Tax Compliance Enhancement

The auto generation of IRN numbers creates tamper-proof transaction records that prevent fake invoice generation a primary mechanism for fraudulent ITC claims under the previous system. With every invoice issued entering the central tax database immediately, tax authorities detect mismatches between supplier declarations and recipient claims in real-time rather than months later during audit cycles.

Real-time data availability enables the GST council to monitor transaction patterns across sectors, identify potential tax evasion networks, and target enforcement resources effectively. The systemic approach reduces revenue leakage that manual verification could never address at scale.

Business Process Improvements

Auto population of GSTR-1 eliminates manual errors in return preparation, ensuring consistency between issued invoices and declared supplies. The standard format across all notified taxpayers simplifies document exchange between supply chain partners recipients can verify authenticity by scanning the QR code rather than conducting manual checks.

Supply chain transparency improves when all business to business transactions carry verifiable authentication. Payment cycles often accelerate because buyers accept compliant invoices without dispute, and financing institutions can verify invoice legitimacy against the e way bill generation records and IRP database when considering invoice discounting or supply chain financing.

Penalties for Non-Compliance

The CGST Act establishes clear consequences for e-invoicing failures, making compliance economically essential.

Under Section 122 of CGST Act, 2017, failing to generate required e-invoices triggers penalties of the higher of Rs. 10,000 per invoice or 100% of the tax amount involved. For small businesses, even a single missed invoice can create disproportionate financial impact.

Issuing invoices with incorrect mandatory fields resulting in invalid IRN or missing QR code attracts penalties of Rs. 25,000 per incorrect invoice. These penalties apply regardless of whether the underlying supply was legitimate and properly taxed.

Additional consequences include:

- Goods in transit without valid e-invoice documentation face detention under Section 129 of CGST Act

- Buyers cannot claim input tax credit for invoices lacking proper IRN, creating commercial disputes

- Repeated non-compliance triggers compliance notices, potential audits, and increased scrutiny of all tax positions

- Invoice issued without valid IRN holds no standing for GST purposes regardless of payment status

Time Limit and Compliance

Reporting Deadlines and Compliance Cycles

Timely reporting of e-invoices is a cornerstone of GST compliance, ensuring that every invoice issued by notified taxpayers is validated and authenticated within the prescribed time frame. With the latest advisory from GSTN, effective April 1, 2025, businesses must upload their e invoice details to the Invoice Registration Portal (IRP) within 30 days from the date of invoice generation. This time limit applies to all eligible invoices, including those with significant invoice value and taxable value, and is crucial for maintaining a seamless compliance cycle.

The compliance workflow begins with the preparation of the e invoice in your billing software, ensuring all mandatory fields are completed. Once ready, the invoice is uploaded to the IRP via the e invoice portal, where it undergoes real-time validation. Upon successful verification, the IRP assigns a unique invoice reference number (IRN) and returns a digitally signed response, complete with a QR code. This authenticated invoice is then automatically reported to the GST portal, enabling auto generation of GST returns and reducing the risk of manual errors.

Auto reporting and auto generation features built into the GST system and e invoice portal streamline the entire process, allowing businesses to focus on accuracy and efficiency. By adhering to the 30-day time limit, businesses ensure that every invoice is legally valid, supports input tax credit claims, and aligns with the compliance cycles mandated by GST law. Staying within this reporting window is especially critical for businesses with high aggregate turnover, as it minimizes compliance risks and supports uninterrupted business operations.

Consequences of Delayed Reporting

Missing the 30-day reporting window for e-invoice submission can have significant repercussions for businesses, particularly those with annual turnover or aggregate turnover above the prescribed threshold. Under the GST system, any invoice not reported to the Invoice Registration Portal IRP within the stipulated time limit is automatically rejected, rendering it invalid for GST purposes.

The consequences of delayed reporting extend beyond simple rejection. Notified taxpayers who fail to obtain a valid IRN for their invoices face penalties as outlined in Rule 48 of the CGST Act, 2017 up to ₹10,000 or 100% of the tax involved per invoice, whichever is higher. Additionally, incorrect or incomplete invoices may attract further penalties of ₹25,000 per document. These financial penalties can quickly add up, especially for businesses with high transaction volumes.

Operationally, invoices without a valid IRN are not recognized by the GST system, meaning recipients cannot claim Input Tax Credit (ITC) on such invoices. This can disrupt business relationships and cash flow, as buyers may refuse to process payments for non-compliant documents. Furthermore, goods transported without proper e-invoice documentation risk detention under GST law, with the e way bill and e way bill portal cross-verifying the presence of a valid IRN.

To avoid these consequences, businesses must prioritize timely e-invoice reporting, leveraging the auto reporting and auto generation capabilities of their billing software and the GST portal. By maintaining strict adherence to compliance cycles and the prescribed threshold, notified taxpayers can safeguard their operations, minimize exposure to penalties, and ensure every invoice issued is fully compliant and recognized by tax authorities.

Why Choose LOGIC ERP for E-Invoicing Process?

LOGIC ERP stands out as a comprehensive solution for businesses navigating the complexities of GST e-invoicing. Designed to seamlessly integrate with the government’s Invoice Registration Portal (IRP), LOGIC ERP automates the entire e-invoicing workflow from invoice creation to IRN generation and QR code embedding ensuring full compliance with GST regulations. Its user-friendly interface supports real-time validation of mandatory fields, reducing errors and minimizing the risk of invoice rejection.

With LOGIC ERP, businesses benefit from robust API connectivity that facilitates instant data transmission to the IRP, accelerating invoice authentication and streamlining return filing through auto-population features. The platform also offers advanced reporting and audit trails, enabling companies to monitor e-invoice statuses and maintain accurate records effortlessly.

Moreover, LOGIC ERP’s scalable architecture caters to enterprises of all sizes, accommodating high transaction volumes without compromising performance. Its integration capabilities extend beyond e-invoicing, linking seamlessly with e-way bill generation and GST return filing modules to provide an end-to-end compliance ecosystem.

Choosing LOGIC ERP not only ensures adherence to evolving e-invoicing rules but also enhances operational efficiency, reduces manual workload, and supports sustainable business growth through digital transformation.

Additional Resources

Official GSTN guidelines: Access the e invoice portal at einvoice.gst.gov.in for current schema specifications, validation rules, and master data references including HSN codes and state-PIN mapping files.

Form GST INV 01 reference: The mandatory field guide details all 28 absolutely mandatory fields plus conditional requirements based on transaction type essential documentation for billing software configuration.

LOGIC ERP integration capabilities: For businesses seeking streamlined e-invoicing compliance, LOGIC ERP offers built-in IRP connectivity, automatic JSON format generation from standard invoicing workflows, validation checks before submission, and integrated e way bill generation for goods transport documentation.

Conclusion and Next Steps

E-invoicing represents mandatory GST compliance for all registered persons exceeding the Rs. 5 crore aggregate turnover threshold, requiring government authentication through the Invoice Registration Portal before any B2B invoice becomes legally valid. The system’s real-time verification, automatic return population, and unique invoice reference number assignment create an integrated compliance framework that traditional invoicing cannot replicate.

Immediate action items:

- Assess your turnover against the prescribed threshold across all GSTINs under your PAN since FY 2017-18

- Evaluate current billing software capabilities for e invoice schema compliance and IRP API connectivity

- Prepare technical infrastructure including JSON format generation and validation testing

- Train relevant staff on mandatory fields, time limit requirements, and error resolution procedures

- Establish IRP connectivity and verify successful IRN generation before compliance deadlines apply

- Assess your specific business needs, including statutory requirements, when customizing e-invoicing implementation such as QR code placement or content to ensure compliance and operational efficiency.

Related exploration topics: E way bill integration with e-invoice data for goods transport, GST return automation leveraging auto population features, and digital invoice management systems that centralize compliance documentation.

Call at +91-73411-41176 or send us an email at sales@logicerp.com to book a free demo today!

Frequently Asked Questions (FAQs)

1. What is e-invoicing under GST?

E-invoicing under GST is the process where businesses electronically report their B2B invoices to the government’s Invoice Registration Portal (IRP) to obtain a unique Invoice Reference Number (IRN). This authentication ensures that the invoice is legally valid and compliant with GST regulations.

2. Who is required to comply with e-invoicing rules?

E-invoicing is mandatory for registered persons whose aggregate turnover exceeds Rs. 5 crore in any preceding financial year from 2017-18 onwards. This includes businesses making B2B supplies, exports, and supplies to government departments, excluding certain exempted entities.

3. What are the benefits of implementing e-invoicing?

E-invoicing enhances tax compliance by reducing errors and preventing fraudulent invoices. It streamlines business processes by enabling automatic reporting to GST returns, accelerates payment cycles, reduces processing costs, and supports sustainability by cutting paper usage by up to 90%.

4. What happens if a business does not comply with e-invoicing regulations?

Non-compliance can attract penalties up to ₹10,000 or 100% of the tax amount, whichever is higher, per invoice. Issuing incorrect invoices may result in penalties of ₹25,000 per invoice. Additionally, invoices without a valid IRN are invalid for claiming input tax credit, leading to financial losses.

5. How soon must an invoice be reported to the IRP?

From April 1, 2025, notified taxpayers with turnover above Rs. 10 crore must report invoices within 30 days from the invoice date. Failure to comply results in invoice rejection and invalidity under GST law.

6. Can e-invoices be amended after IRN generation?

No, amendments are not allowed on the IRP after IRN generation. Corrections must be made during GST return filing, and cancellations can be requested within 24 hours of IRN generation, subject to certain conditions.

7. Is e-invoicing applicable to B2C transactions?

No, e-invoicing currently applies only to Business-to-Business (B2B) transactions and exports by notified taxpayers. B2C sales and certain exempt transactions are excluded.

8. How does e-invoicing improve GST return filing?

E-invoicing auto-populates invoice data into GST returns such as GSTR-1, minimizing manual entry errors and ensuring timely and accurate compliance with tax authorities.

9. What are the mandatory data fields in an e-invoice?

Mandatory fields include supplier and recipient GSTIN, invoice number and date, HSN/SAC codes, taxable value, tax rates, and invoice value. Accurate completion of these fields is essential for IRP validation and IRN generation.

10. How can LOGIC ERP help with e-invoicing compliance?

LOGIC ERP offers seamless integration with the IRP, automating invoice data submission, validation, and IRN generation. Its robust features reduce errors, ensure timely compliance, and streamline GST return filing, making it an ideal solution for businesses navigating e-invoicing requirements.

11. What is E-Invoicing?

E-invoicing under GST is the process where businesses electronically report their B2B invoices to the government’s Invoice Registration Portal (IRP) to obtain a unique Invoice Reference Number (IRN). This authentication ensures that the invoice is legally valid and compliant with GST regulations, enabling seamless tax compliance and input tax credit claims.

12. How to Generate E-Invoice?

To generate an e-invoice, a registered person must prepare the invoice in their billing software with all mandatory fields, then upload the invoice data in JSON format to the IRP via API or offline utility. Upon validation, the IRP returns a digitally signed e-invoice with a unique IRN and QR code, which must be issued to the recipient.

13. How to Cancel E-Invoice?

E-invoices can be canceled within 24 hours of IRN generation by submitting a cancellation request through the IRP’s API or portal. Cancellation is subject to conditions such as no active e-way bill linked to the invoice. After cancellation, the invoice number cannot be reused.

14. What is E-Invoicing in GST?

E-invoicing in GST mandates that certain registered taxpayers electronically report their B2B invoices to the IRP for real-time validation and authentication, ensuring standardized invoice formats and reducing tax evasion.

15. Can E-Invoice Be Generated After Invoice Date?

Yes, e-invoices must be reported to the IRP within 30 days from the invoice generation date as per GSTN advisory effective April 1, 2025. Generating e-invoices after this period is not permitted and will be rejected.

16. How to Generate E-Invoice in GST Portal?

Businesses can generate e-invoices on the GST portal by uploading invoice data in the prescribed format through APIs, GST Suvidha Providers (GSPs), or using the offline bulk upload utility provided on the e-invoice portal.

17. How to Make E-Invoice?

E-invoices are created by preparing the invoice with all mandatory details in accounting or ERP software, then submitting the data to the IRP for validation and IRN generation. The authenticated invoice with QR code is then issued to the buyer.

18. How to Create E-Invoice?

Creating an e-invoice involves entering invoice particulars in compliance with the GST e-invoice schema, transmitting the data to the IRP, receiving the IRN and signed JSON response, and sharing the authenticated invoice with the recipient.

19. Is E-Invoicing Mandatory?

Yes, e-invoicing is mandatory for registered persons with aggregate turnover exceeding Rs. 5 crore in any preceding financial year from 2017-18 onwards, for B2B supplies and exports.

20. What is E-Invoicing Under GST?

E-invoicing under GST is the electronic reporting and authentication of business invoices through the IRP, which assigns a unique IRN and generates a digitally signed invoice with a QR code, making it valid for GST compliance.

21. Can E-Way Bill Be Generated After Invoice Date?

Yes, an e-way bill can be generated after the invoice date but must be generated before the movement of goods begins. The invoice date and e-way bill date can differ, but timely generation is critical for compliance.

22. Is E-Way Bill Required for Service Invoice?

No, e-way bills are generally not required for service invoices as they apply to the movement of goods. However, if goods are transported in relation to services, e-way bills may be necessary.

23. Can I Generate One E-Way Bill for Two Invoices?

Yes, a single e-way bill can be generated for multiple invoices if the goods are transported together in one conveyance and the transporter details are common.

24. Can We Generate Multiple E-Way Bills for Single Invoice?

Yes, multiple e-way bills can be generated for a single invoice if goods are transported in multiple consignments or vehicles.

25. How to Change Invoice No in E-Way Bill?

Invoice number cannot be changed once the e-way bill is generated. To correct invoice details, the e-way bill must be canceled and a new one generated with the correct invoice number.

26. How to Generate E-Way Bill for Bulk Invoices?

Bulk e-way bills can be generated using the bulk upload facility on the e-way bill portal by uploading a CSV or Excel file containing invoice and transport details, streamlining compliance for large consignments.

27. What is E-Invoicing in India?

E-invoicing in India is a GST compliance mechanism where specified taxpayers must electronically report B2B invoices to the government’s IRP for real-time validation, authentication, and issuance of a unique IRN.

28. Can Invoice Date and E-Way Bill Date Be Different?

Yes, the invoice date and e-way bill date can differ; however, the e-way bill must be generated before the commencement of goods movement to ensure compliance.

29. Can We Generate Single E-Way Bill for Multiple Invoices?

Yes, a single e-way bill can cover multiple invoices if the goods are transported together under the same conveyance and transporter details.

30. Can We Make One E-Way Bill for Multiple Invoices?

Yes, it is permitted to generate one e-way bill for multiple invoices provided the transportation conditions are met as per GST rules.

31. How to Add Multiple Invoices in E-Way Bill?

Multiple invoices can be added in the e-way bill portal by selecting the bulk upload option or manually entering invoice details in the e-way bill creation form.

32. How to Change Invoice Date in E-Way Bill?

Invoice date cannot be changed after e-way bill generation. To correct it, the e-way bill must be canceled and a new one created with the correct details.

33. How to Change Invoice Number in E-Way Bill?

Changing the invoice number post-generation is not allowed. Cancellation of the existing e-way bill and re-creation with correct invoice details is required.

34. How to Check E-Way Bill by Invoice Number?

You can check e-way bill details by invoice number on the e-way bill portal’s search feature by entering the invoice number and other relevant details.

35. How to Generate E-Invoice in GST?

E-invoices are generated by preparing invoice data in the prescribed format and submitting it to the IRP via API, GSP, or offline utility for validation and IRN issuance.

36. How to Generate E-Invoice Under GST?

Under GST, e-invoices are generated by uploading invoice details to the IRP, which validates and returns a signed invoice with a unique IRN and QR code for compliance.

37. How to Generate E-Way Bill for Multiple Invoices?

Generate an e-way bill for multiple invoices by using the bulk upload feature on the e-way bill portal or by entering multiple invoice details under one e-way bill if goods are transported together.

38. How to Generate One E-Way Bill for Multiple Invoices?

One e-way bill can be generated for multiple invoices if the goods are transported in a single conveyance, using the bulk upload or manual entry option on the portal.

39. How to Generate Single E-Way Bill for Multiple Invoices?

The process involves selecting multiple invoices during e-way bill creation on the portal or uploading a bulk file containing all invoice details for combined transportation.

40. How to Make E-Way Bill for Multiple Invoices?

Use the bulk upload feature or manual entry on the e-way bill portal to consolidate multiple invoices into a single e-way bill for goods transported together.

41. What is E-Invoice System?

The e-invoice system is a government-mandated electronic platform where B2B invoices are reported, validated, and authenticated via the Invoice Registration Portal to ensure GST compliance and prevent tax evasion.

42. What is E&OE in an Invoice?

E&OE stands for “Errors and Omissions Excepted,” a disclaimer on invoices indicating that the issuer is not responsible for minor errors or omissions and reserves the right to correct them.

43. Why E-Invoicing?

E-invoicing enhances tax compliance, reduces fraudulent invoices, streamlines GST return filing through auto-population, improves payment cycles, and supports sustainable business practices by reducing paper usage.

44. How Does E-Invoicing Work?

E-invoicing works by having businesses upload invoice data to the IRP, which validates the details, generates a unique IRN and QR code, and returns a digitally signed invoice, ensuring authenticity and legal validity.

45. How E-Invoicing Works?

The process involves invoice creation in billing software, data submission to the IRP, real-time validation, IRN generation, and issuance of an authenticated invoice to the buyer, integrated with GST return filing.

46. How to Generate Multiple E-Way Bills for Single Invoice?

Multiple e-way bills for a single invoice can be generated when goods are dispatched in several consignments using different vehicles or routes, each requiring a separate e-way bill.

47. What is E-Invoice System in GST?

The GST e-invoice system is the electronic mechanism for authenticating B2B invoices through the IRP, ensuring standardized invoice formats, real-time validation, and seamless integration with GST returns and e-way bills.

Author

Gurbir Singh

Co-founder & Managing Director | LOGIC ERP Solutions Pvt. Ltd.

With 30+ years of experience in the tech industry, I took the helm of technology & product development, ensuring LOGIC ERP’s continuous innovation & leadership in the evolving tech landscape.