How to Record Bills Receivable in Trial Balance & Final Accounts

Summary

Learn how bills receivable are recorded in the trial balance and final accounts with proper journal entries, balance sheet classification, and accounting treatment. This guide explains the difference between bills receivable and accounts receivable, handling dishonoured bills, common accounting errors, and how LOGIC ERP simplifies bills receivable management with automation, tracking, and real-time financial visibility.

Contact Us

Free Demo Request

Table of Contents

- Introduction

- Understanding Bills Receivable in Accounting Context

2.1 Bills Receivable vs Accounts Receivable

2.2 Trial Balance Fundamentals - Recording Bills Receivable in Books of Accounts

3.1 Initial Recognition and Journal Entries

3.2 Subsequent Measurement Events

3.3 Special Transactions - Bills Receivable in Trial Balance Preparation

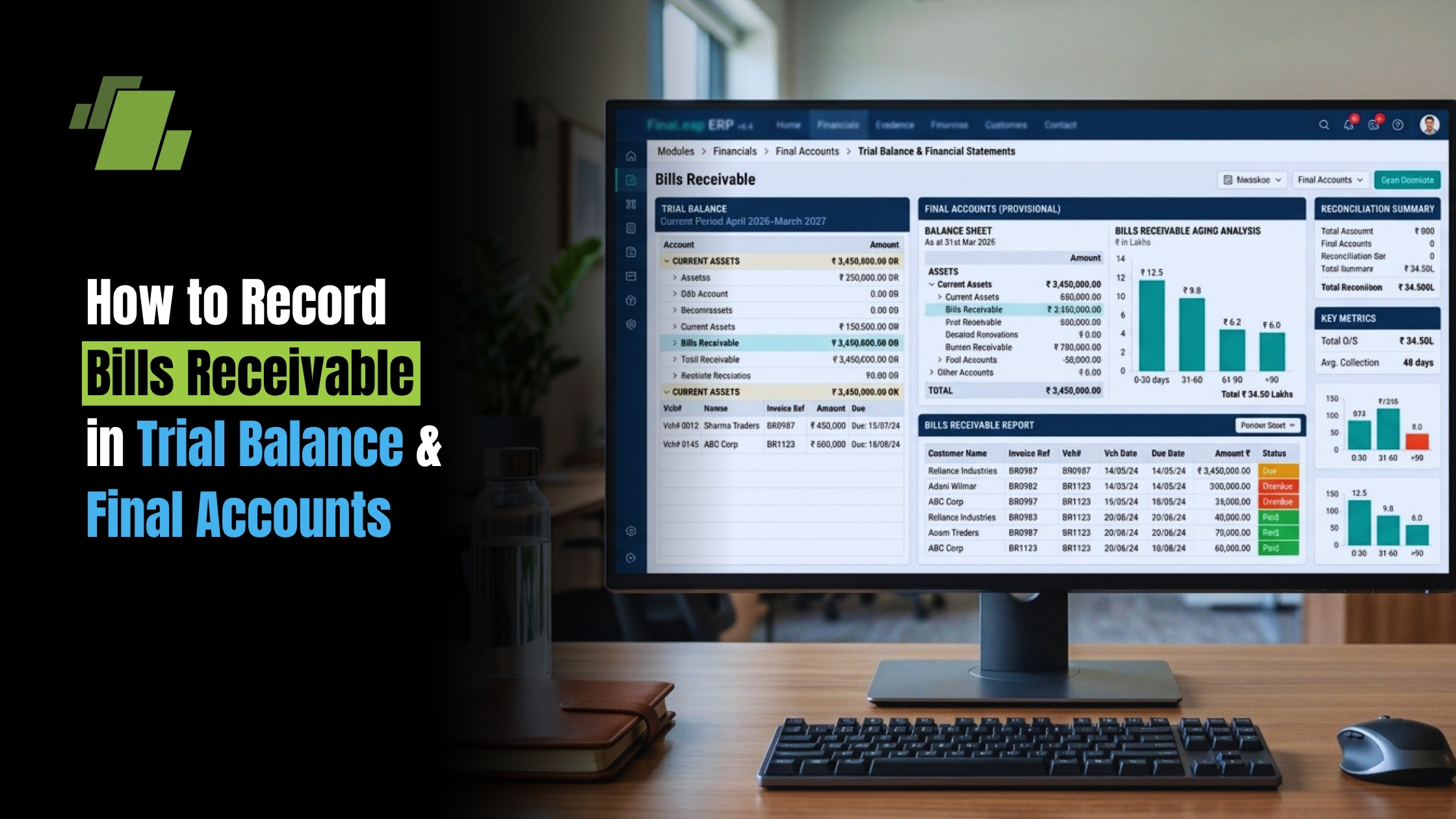

4.1 Trial Balance Placement and Classification

4.2 Trial Balance Format and Example - Transfer to Final Accounts

5.1 Balance Sheet Presentation

5.2 Profit & Loss Account Considerations

5.3 Notes to Financial Statements - Common Challenges and Solutions

6.1 Incorrect Trial Balance Placement

6.2 Dishonoured Bills Treatment

6.3 Year-end Cutoff Issues

6.4 Maturity Classification Errors - What Features Does LOGIC ERP Offer to Simplify the Management of Bills Receivable?

- Conclusion and Next Steps

- Frequently Asked Questions (FAQs)

Introduction

Bills receivable are negotiable instruments representing money owed by customers for credit sales, and they require precise recording in your trial balance to ensure accurate financial statements. A bill receivable is a bill of exchange drawn by a vendor on its customer, serving as proof of debt and a legal arrangement for debt recovery. Understanding how to properly record these receivable bills determines whether your accounting period closes with balanced books and correct asset classifications.

This guide covers trial balance recording procedures, final accounts preparation, and essential journal entries for bills receivable transactions. We exclude advanced discounting techniques and complex financial derivatives, focusing instead on practical recording methods. The target audience includes accounting students learning foundational concepts, bookkeepers managing daily transactions, and small business owners who need to prepare financial statements accurately.

Direct answer: Bills receivable are recorded as current assets in the trial balance under the debit column and transferred to the balance sheet as receivables, classified based on their maturity date.

By working through this content, you will:

- Master journal entry formats for creating, honoring, and handling dishonored bills

- Understand precise trial balance placement for the bills receivable account

- Learn to prepare accurate final accounts with proper asset classification

- Identify and avoid common recording errors that affect financial health

Understanding Bills Receivable in Accounting Context

Bills receivable represent amounts owed to a business by its customers for goods or services sold on credit, typically due within a short period such as 30, 60, or 90 days. When a customer accepts a bill receivable, it becomes a current asset for the seller, reflecting the amount owed to them for credit sales. This formal written promise creates stronger legal enforceability than standard accounts receivable entries.

The asset nature of bills receivable means they appear on the debit side of your ledger. Classification as current or non-current depends on the maturity account receivable dr timing bills due within twelve months of the balance sheet date qualify as current assets, while long term bills extending beyond this period require classification as non current assets.

1. Bills Receivable vs Accounts Receivable

Accounts receivable arise from informal credit sales where customers receive goods or services sold with agreed payment terms but without formal documentation beyond invoices. Bills receivable, by contrast, are formal negotiable instruments specifically bills of exchange or promissory notes that create binding legal obligations with explicit due date specifications.

The legal enforceability differences are substantial. When a customer fails to pay accounts receivable, collection efforts rely on general commercial law. Bills receivable, however, carry specific statutory protections and clearer procedures for legal action, including noting charges that document non payment formally. Documentation requirements for bills include acceptance signatures, specific principal amount, maturity date, and other terms that strengthen the creditor’s position in any dispute.

2. Trial Balance Fundamentals

A trial balance is a list of all ledger account balances at the end of an accounting period, organized with debit balances in one column and credit balances in another. Its primary purpose is verifying arithmetic accuracy before you prepare financial statements if total debits equal total credits, the books are mathematically balanced (though not necessarily error-free in terms of correct account classifications).

The trial balance serves as the bridge between your company’s books of individual transactions and the final accounts. Every asset, liability, revenue, and expense account appears here, making it essential to place bills receivable correctly before transferring amounts to your balance sheet and profit and loss statements.

Recording Bills Receivable in Books of Accounts

With foundational concepts established, recording procedures follow a logical sequence from initial recognition through subsequent events. Each transaction type requires specific accounting entries that maintain the integrity of your receivable accounts.

1. Initial Recognition and Journal Entries

When a business creates a bill receivable, it records the transaction by debiting the bills receivable account and crediting the sales account (or accounts receivable if converting an existing debt), reflecting the recognition of revenue and an asset.

The standard journal entry for drawing a bill on a customer converting an existing debt:

Bills Receivable A/c Dr. [Amount]

To Accounts Receivable A/c Cr. [Amount]

This entry transfers the pending amount from informal receivable to formal negotiable instrument. The customer’s acceptance creates binding payment obligations, and your records reflect a potentially more collectible asset due to the enhanced legal standing of bills versus unpaid invoices.

2. Subsequent Measurement Events

Upon receiving payment for a bill receivable, the business debits cash or bank and credits the bills receivable account to close the entry and reflect the inflow of cash. The honour entry appears as:

Bank/Cash A/c Dr. [Amount]

To Bills Receivable A/c Cr. [Amount]

This cash inflow improves your working capital position and eliminates the receivable from your books.

If a bill receivable is dishonored, the amount is transferred back to accounts receivable, and the journal entry reflects this by debiting accounts receivable and crediting bills receivable. Noting charges paid to document the dishonor add to the customer’s debt:

Accounts Receivable A/c Dr. [Bill Amount + Noting Charges]

To Bills Receivable A/c Cr. [Bill Amount]

To Cash/Bank A/c Cr. [Noting Charges Paid]

3. Special Transactions

Discounting with bank occurs when you need immediate funds rather than waiting until maturity. The bank advances cash minus discount charges:

Bank A/c Dr. [Amount Received]

Discount Charges A/c Dr. [Discount Amount]

To Bills Receivable A/c Cr. [Face Value]

This transaction accelerates your cash flow but reduces total collection by the interest charged. If the customer later dishonors the discounted bill, you must handle the dishonor entry and potentially repay the bank, creating additional complexity in your records.

Key points: Bills receivable maintain their asset nature throughout their lifecycle until honored or written off as bad debt. Timing recognition follows acceptance date for initial recording and due date for maturity-related classifications.

Bills Receivable in Trial Balance Preparation

Building on journal entry knowledge, trial balance placement requires systematic verification to ensure all the bills appear correctly before final accounts preparation.

1. Trial Balance Placement and Classification

Bills receivable appear in the trial balance when outstanding balances exist at period-end that is, when customers have accepted bills that remain unpaid as of your closing date. Follow these steps for accurate placement:

- Identify outstanding bills receivable at period-end by reviewing your bills receivable account ledger and any subsidiary schedules listing individual bills with their invoice date, maturity date, and pending payment status.

- Record total bills receivable balance in the debit column of the trial balance. Since receivable represent amounts owed to your company, they maintain debit balances throughout their existence as assets.

- Verify amounts match supporting schedules by reconciling the ledger total against detailed listings of individual bills. Multiple bills should sum to the trial balance figure without discrepancy.

- Ensure proper classification between current and non-current portions by analyzing maturity dates relative to your balance sheet date. Bills due within twelve months belong with current assets; those extending beyond require separate non-current treatment.

2. Trial Balance Format and Example

The following trial balance extract demonstrates proper bills receivable placement:

| Particulars | Debit (₹) | Credit (₹) |

|---|---|---|

| Cash/Bank A/c | 45,000 | – |

| Bills Receivable A/c | 75,000 | – |

| Accounts Receivable A/c | 120,000 | – |

| Inventory A/c | 200,000 | – |

| Bills Payable A/c | – | 50,000 |

| Sales A/c | – | 500,000 |

| Purchases A/c | 300,000 | – |

| … | … | … |

The debit bills entry of ₹75,000 reflects all outstanding bills held at period-end. This amount represents a current asset assuming all bills mature within the upcoming financial year. The synthesis for readers: bills receivable always appear in the debit column because they represent asset money that customers owe your business.

Transfer to Final Accounts

Transitioning from trial balance to final accounts involves transferring bills receivable to appropriate financial statements classifications and recognizing any related income or expense items in the profit and loss account.

1. Balance Sheet Presentation

Bills receivable appear under current assets for bills due within twelve months of your balance sheet date. Standard presentation shows them after or alongside accounts receivable, often combined under “Trade Receivables” with detailed notes:

Current Assets:

- Trade Receivables

- Accounts Receivable: ₹120,000

- Bills Receivable: ₹75,000

- Cash and Bank: ₹45,000

For bills extending beyond the twelve-month threshold, classify the non-current portion separately. This distinction matters significantly for cash flow forecasting and liquidity analysis stakeholders assessing your financial health expect accurate current versus non-current splits.

Bills receivable can block funds until their maturity, creating liquidity risks and opportunity costs for businesses that could otherwise invest those funds. Proper balance sheet presentation communicates these timing factors to readers of your financial statements.

2. Profit & Loss Account Considerations

Interest income recognition applies when bills bear explicit interest rates. Record interest earned in your profit and loss account as financial income, separate from operating revenue:

Interest Receivable A/c Dr.

To Interest Income A/c Cr.

Bad debts can occur if market or industry conditions change, reducing a customer’s ability to repay their bills receivable, which can negatively impact the creditor’s financial health. Provisions for doubtful bills receivable reduce your asset carrying value and appear as expenses in the profit and loss account, improving the accuracy of your stated receivable position.

3. Notes to Financial Statements

Disclosure requirements include:

- Total bills receivable balance with maturity analysis showing due dates across time bands

- Any bills discounted with bank and associated contingent liabilities if recourse exists

- Credit terms offered to customers and aging of receivables

- Provisions maintained for doubtful collection

- Related party transactions involving bills receivable

These notes support stakeholder understanding of your business operations and credit management practices, fulfilling transparency requirements under various accounting standards.

Common Challenges and Solutions

Recording bills receivable correctly presents several typical difficulties. Understanding these challenges and their solutions strengthens your accounting accuracy.

1. Incorrect Trial Balance Placement

Some practitioners mistakenly credit bills receivable or place them under liabilities, causing trial balance imbalance or misstatement of assets and liabilities.

Solution: Always record bills receivable in the debit column because they represent assets amounts customers owe your company. Double-check entries against the fundamental accounting equation: assets equal liabilities plus equity, and all asset increases are debits.

2. Dishonoured Bills Treatment

Failure to properly reverse bills receivable when dishonored, or neglecting noting charges, leaves incorrect balances in multiple accounts.

Solution: Transfer dishonoured amounts back to accounts receivable with proper notation of noting charges cr and additional fees. The risk of default occurs when a debtor fails to pay the bill receivable, leading to potential financial loss for the creditor accurate recording ensures your receivable accounts reflect actual collectible amounts.

3. Year-end Cutoff Issues

Bills accepted near period-end may be overlooked or recorded in the wrong accounting period, causing understated or overstated assets.

Solution: Verify all bills issued before year-end are recorded regardless of acceptance date. Review transaction logs and correspondence around period-end dates to capture pending acceptances that belong in the current period.

4. Maturity Classification Errors

Incorrectly classifying long term bills as current assets (or vice versa) distorts liquidity ratios and working capital calculations.

Solution: Analyze maturity dates systematically to correctly classify between current and non-current assets. Create a maturity schedule listing each bill with its due date, then apply the twelve-month threshold consistently from your balance sheet date.

What Features Does LOGIC ERP Offer to Simplify the Management of Bills Receivable?

LOGIC ERP accounting software offers comprehensive features to simplify bills receivable management by automating tracking and classification processes. Key functionalities include individual bill tracking with acceptance and maturity dates, automated alerts for due bills, and integration with cash flow forecasting tools. The system supports subsidiary ledger management, enabling detailed aging analysis and Days Sales Outstanding (DSO) calculations. It also facilitates dishonor tracking with noting charges recording, ensuring accurate financial reporting. These features help businesses improve cash flow, reduce bad debts, and maintain precise trial balance and final accounts records.

Conclusion and Next Steps

Bills receivable maintain their debit nature throughout the accounting cycle, appearing in trial balance as assets and transferring to balance sheet under current assets (or non-current for longer maturities). Effective management of bills receivable can lead to improved cash flow, reduced bad debt, and enhanced financial stability for businesses. Monitoring Days Sales Outstanding (DSO) is crucial for assessing the average collection period of bills receivable, which helps in managing cash flow effectively.

Immediate action steps:

- Review your current bills receivable ledger for accuracy and completeness

- Verify trial balance placement shows debit balances matching your subsidiary schedules

- Prepare supporting schedules listing all bills with maturity analysis for financial statement preparation

- Implement regular follow-up procedures to manage cash and minimize dishonor risk

Best practices for managing bills receivable include timely invoicing, clear payment terms, regular follow-ups, and conducting credit checks on customers. Dispute risks arise when the terms of the bill receivable are not clearly stated, potentially leading to legal actions to enforce payment clear documentation prevents these complications.

Related topics worth exploring include bills payable treatment (the liability counterpart), provision for doubtful debts calculations, and cash flow statement impact of receivable movements.

Call at +91-73411-41176/75 or send us an email at sales@logicerp.com to book a free demo today!

Frequently Asked Questions (FAQs)

1. How Is The Account Receivable Balance Related To Bills Receivable?

The account receivable balance includes all amounts owed by customers, comprising both informal credit sales and formal bills receivable. When a bill receivable is drawn and accepted, the corresponding amount is transferred from accounts receivable to bills receivable, reflecting a legally enforceable debt. This distinction helps businesses track credit sales more precisely and manage collections effectively.

2. What Is The Journal Entry For Bills Receivable On Credit Purchases?

Credit purchases generate bills payable rather than bills receivable. However, when recording bills receivable related to credit sales, the journal entry involves debiting the bills receivable account and crediting sales or accounts receivable. For credit purchases, the entry debits purchases and credits bills payable. This separation ensures accurate classification of assets and liabilities in the trial balance and final accounts.

3. How Does Foreign Exchange Affect Bills Receivable?

Foreign exchange fluctuations impact bills receivable denominated in foreign currency. The value of such bills must be remeasured at the reporting date using the prevailing exchange rate, which can result in foreign exchange gains or losses recognized in the profit and loss account. Proper accounting for foreign exchange ensures compliance with international financial reporting standards and accurate financial statements.

4. What Role Does The Months Bank Dr Play In Bills Receivable Management?

The term “months bank dr” refers to the debit balance in the bank account related to discounted bills receivable. When a business discounts a bill with the bank before maturity, the bank advances cash minus discount charges, creating a debit balance. Monitoring this figure is essential for managing cash flow and reconciling discounted bills in the accounting records.

5. In What Various Forms Can Bills Receivable Exist?

Bills receivable can take various forms, including bills of exchange, promissory notes, and negotiable instruments. Each form carries specific legal and accounting implications but generally serves as proof of debt owed by customers. Understanding these forms helps businesses choose appropriate documentation for credit transactions and ensures proper recording in trial balance and final accounts.

6. How Can A Business Effectively Collect Bills Receivable?

Effective collection of bills receivable involves timely invoicing, clear payment terms, regular follow-ups, and credit checks on customers. Utilizing automated reminders and maintaining accurate subsidiary ledgers aid in monitoring due dates and outstanding amounts. Prompt collection improves cash flow, reduces bad debts, and strengthens financial stability.

7. What Happens If A Bill Receivable Is Dishonored?

If a bill receivable is dishonored, the amount is transferred back to accounts receivable, and any noting charges incurred are added to the customer’s debt. The journal entry debits accounts receivable and credits bills receivable, with noting charges debited to expenses or added to receivables. Proper treatment ensures accurate representation of collectible amounts and legal recourse options.

8. How Are Bills Receivable Presented In The Trial Balance And Final Accounts?

Bills receivable appear as current assets in the debit column of the trial balance when outstanding at period-end. In final accounts, they are classified under current assets in the balance sheet, with maturity analysis disclosed in notes. Correct presentation aids stakeholders in assessing liquidity and credit management effectiveness.

9. Why Is Monitoring Days Sales Outstanding (DSO) Important For Bills Receivable?

Monitoring DSO helps businesses assess the average collection period for bills receivable, revealing efficiency in credit management. Lower DSO indicates quicker collections and improved cash flow, while higher DSO may signal collection issues or credit risk. Using DSO metrics supports proactive receivable management and financial planning.

10. How Do Bills Receivable Impact Cash Flow And Financial Stability?

Bills receivable represent expected cash inflows but can block funds until maturity, creating liquidity risks and opportunity costs. Effective management ensures timely collections, reducing bad debts and enhancing financial stability. Accurate recording and monitoring enable businesses to optimize working capital and maintain operational agility.

11. What Is The Journal Entry When Payment Is Received For A Bill Receivable?

Upon receiving payment for a bill receivable, the business debits cash or bank and credits the bills receivable account to close the entry and reflect the inflow of cash.

12. What Are Receivable Bills And How Do They Affect Accounting?

Receivable bills, commonly known as bills receivable, are formal negotiable instruments representing amounts owed to a business by its customers for credit sales. They serve as proof of debt and create legally enforceable claims. In accounting, receivable bills are recorded as assets, reflecting expected future cash inflows.

13. How Is The Bills Receivable Account Maintained In Financial Records?

The bills receivable account is maintained by recording all accepted bills drawn on customers. It is debited when a bill is received and credited when payment is collected or the bill is dishonored. Detailed subsidiary ledgers track individual bills, their maturity dates, and payment status to ensure accurate management.

14. Where Do Bills Receivable Appear On The Balance Sheet?

Bills receivable appear under current assets on the balance sheet if they are due within one year from the reporting date. If bills have maturities beyond one year, they are classified as non-current assets. This classification helps stakeholders assess the company’s liquidity position.

15. What Is The Difference Between Bills Receivable And Bills Payable?

Bills receivable are amounts owed to a business by its customers, representing assets. Bills payable are amounts a business owes to its suppliers or creditors, representing liabilities. Both are formalized by bills of exchange but have opposite impacts on financial statements.

16. What Is The Correct Journal Entry For Recording Bills Receivable?

When a bill receivable is drawn, the journal entry debits the bills receivable account and credits accounts receivable or sales. Upon payment, the cash or bank account is debited, and bills receivable is credited. If dishonored, the amount is transferred back to accounts receivable with appropriate noting charges recorded.

17. How Are Bills Receivable Reflected In Financial Statements?

Bills receivable are reported as assets in the balance sheet, usually under trade receivables or current assets. Interest income from bills bearing interest is recognized in the profit and loss account. Disclosures include maturity analysis and any provisions for doubtful debts related to bills receivable.

18. What Steps Are Involved To Prepare Financial Statements Including Bills Receivable?

Preparation involves verifying the bills receivable ledger for accuracy, reconciling subsidiary schedules with the trial balance, classifying bills as current or non-current based on maturity, recording any necessary provisions, and presenting the amounts correctly in the balance sheet and notes.

19. How Do Bills Receivable Impact A Company’s Cash Flow?

Bills receivable represent expected cash inflows but can block funds until their maturity, affecting liquidity. Effective management, including timely collection and discounting, improves cash flow by converting receivables into cash sooner and reducing the risk of bad debts.

20. How Should Bad Debt Related To Bills Receivable Be Accounted For?

Bad debts from uncollectible bills receivable should be recognized as an expense in the profit and loss account. Provisions for doubtful bills receivable reduce the asset value on the balance sheet, ensuring financial statements reflect realistic collectible amounts.

21. What Are The Common Accounting Entries Associated With Bills Receivable?

Common entries include:

- Debit bills receivable and credit accounts receivable or sales upon drawing the bill.

- Debit cash/bank and credit bills receivable on payment receipt.

- Debit accounts receivable and credit bills receivable if the bill is dishonored.

- Debit discount charges and credit bills receivable when a bill is discounted with a bank.

Author

Gurbir Singh

Co-founder & Managing Director | LOGIC ERP Solutions Pvt. Ltd.

With 30+ years of experience in the tech industry, I took the helm of technology & product development, ensuring LOGIC ERP’s continuous innovation & leadership in the evolving tech landscape.